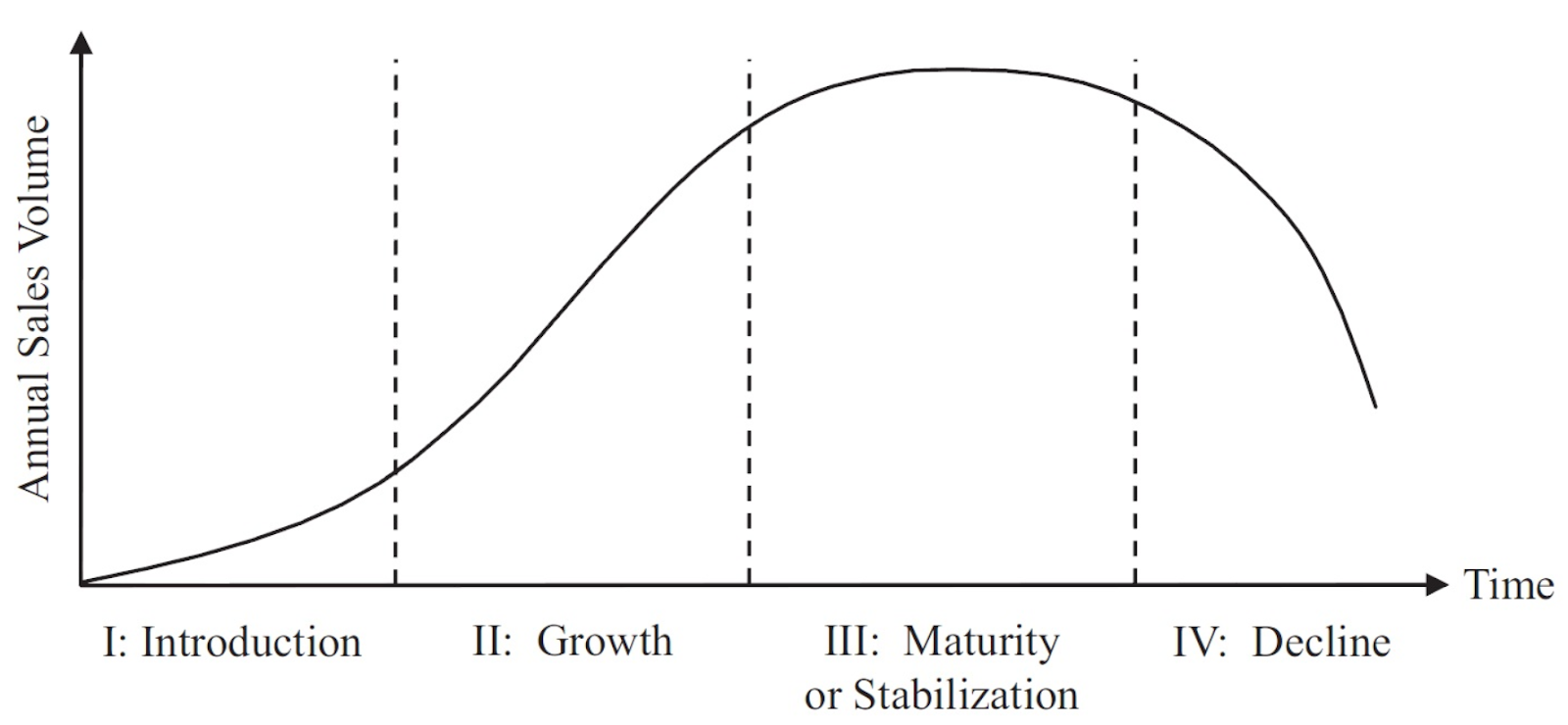

There are markets for just about everything, where sellers and buyers exchange goods and services. The same is true for nursing homes; “sellers” (providers) make their services available to patients and families (consumers) in exchange for payments from the government, or another intermediary (customers). Most markets and services have life cycles; they emerge, they grow, they mature and then, inevitably, they decline.

In the nursing home market, however, no one wants what is being sold. The consumers and the customers need what’s being sold. The need often leaves little or no choice.

After all, nursing homes have two essential value propositions:

- Safer and effective transitions

- Competent custodial care

That’s it!

This is what nursing homes do. There’s hardly anything about these value propositions that’s discretionary. There are some consumers that want the lifestyle opportunities of living in purpose-built assisted-living residences. Nursing home consumers and customers, on the other hand, need nursing home services. Nursing homes manage safer transitions from hospitals back to home and take care of those who cannot take care of themselves.

The good old days: introduction & growth

Modern nursing homes, since their creation by government regulation in the mid 1960s, were supported economically by 10 to 20% of the population who were private pay consumers. These “market rate” consumers cross-subsidized the government Medicaid program, plus those consumers who were unable to pay. This was the “introduction” phase of the nursing home lifecycle. From the mid-1980s, there was a dramatic shift of medical care from hospitals because of prospective payment, toward outpatient care, home care and nursing homes. This redistribution was the result of pressure by the dominant customer (the government) to reduce hospital costs and “bend the healthcare cost curve.” Nursing homes benefited from an influx of higher-acuity and more highly compensated Medicare beneficiaries. Even though Medicare beneficiaries never exceeded 12% of the overall nursing home population, the per-beneficiary compensation was so high that the economic difficulties of the 1990s enabled nursing homes to survive. This could be characterized as the “growth” phase of the nursing home lifecycle.

Then came three shocks: 1. The astringent changes of the Balanced Budget Act of 1997; 2. The decline of the age-qualified population due to the birth-dearth, and; 3. The migratory flight of private pay consumers into assisted-living. The economic consequences of these shocks were softened by Part A Medicare beneficiaries in nursing homes, which kept many of them afloat, and allowed a few to prosper.

The line of decline

The COVID-19 pandemic laid bare the dysfunctional economic underpinnings of the sector. The cross subsidization was abruptly stopped, the underpaid workforce left, and decades of not reinvesting in the infrastructure wreaked deadly consequences.

Continuing neglect now brings reality to the forefront. This is the “decline” phase of the nursing home market.

Markets and services have life cycles; they emerge, they grow, they mature and then, most often, they decline.

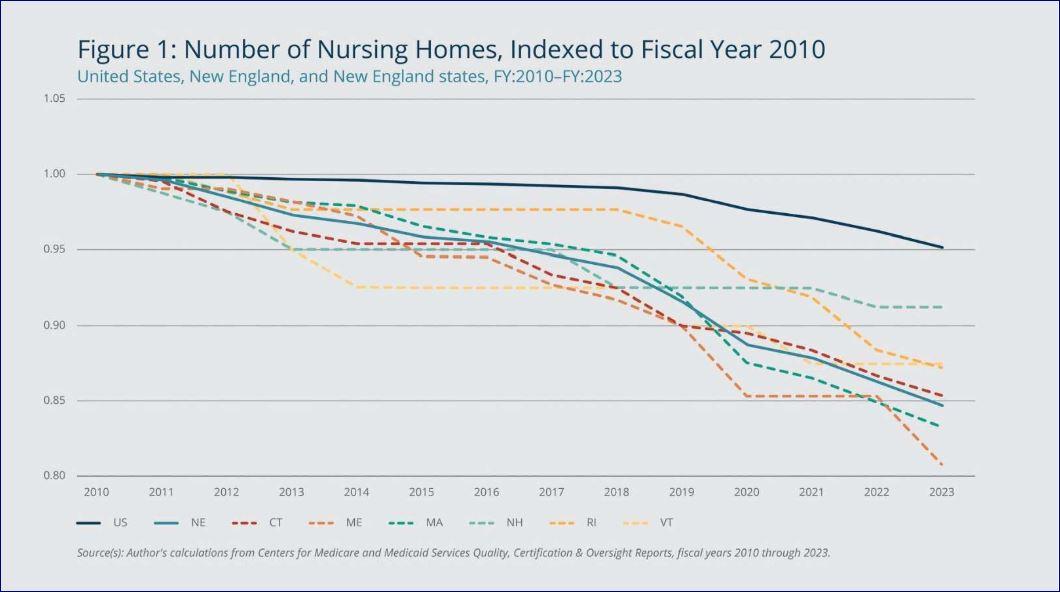

There’s ample evidence of this market decline, including the “contraction” of supply (nursing homes are closing at a rapid rate), “harvesting” of properties by REITs, and the “dropping” of nursing homes through closures.

Here’s the evidence for the decline:

- Nursing homes are broke; as many as 60% of operators are “zombies,” i.e. they cannot survive on their operating income. Evidence of this is all around, especially with measures like days cash on hand, and the rate at which nursing homes are closing due to bankruptcy or to avoid it.

- Most nursing homes are derelict; three decades of financial extraction with little or no substantial reinvestment have left about 70% of properties not fit-for-purpose. Multi-bedded rooms, shared bathrooms, decades-old HVAC and physical infrastructure that are well past their economic life — these are just a few examples.

- Nursing homes are understaffed; the post-pandemic healthcare workforce recovery has bypassed nursing homes as employers of choice. The Bureau of Labor Statistics and other workforce data clearly show that nursing home workforce has not returned to nursing homes after the pandemic shock.,

- Nursing homes are blamed, disparaged and discouraged; the dominant cultural position of the public toward nursing homes is, “Never!” The very first reference to nursing homes in a State of the Union speech by an American president was a threat. The resultant imminent CMS staffing rule is political punishment targeted at the few flagrant profiteers, but more importantly, at the displaced guilt from the ravages of the pandemic, which were the predictable consequences of decades of neglect.

There are “half-full” people, who point quickly to the great services that nursing homes provide, and how important they are to their communities and the healthcare eco-system overall. The current situation in no way negates these facts. And there should be no nostalgia. The sooner and more completely we reconcile ourselves to this inevitable stage of this market lifecycle and its correction, the better for those of us who need to find a way forward.

What that “end of the line” is like, is up to us in the sector, to policy makers and politicians, and to how the underlying consumer and customer needs might be solved in other ways

The needs that survive

Nursing homes provide an economically critical function to society, as well as to the healthcare ecosystem, which cannot be abandoned. Going back to the two inherent value propositions of nursing homes, we can see this.

Transitions of care: Nursing homes facilitate (and lower the risk of) discharges of consumers from acute-care hospitals. Because hospital payments are now overwhelmingly capitated, and progressively more value-based, getting patients out is arguably just as important to a hospital CFO than getting them in. This is a need in the trillion-dollar healthcare ecosystem which will not go away; this is a durable demand. Notably, CMS deployed the Hospital Readmissions Reduction Program (HRRP) in 2012 to penalize hospitals that are out of compliance with readmissions’ standards. In 2018, unnecessary hospital readmissions cost CMS over $57 billion. Over the decade 2010-2019, the HRRP is credited with reducing 30-day and 90-day all-cause readmissions from 12.8% to 11.6%, and 20.6% to 18.8%. In 2023, HRRP fines to hospitals not in compliance still totaled $320 million; these fines are expected to increase in 2024., It is interesting that, even though many SNF managers understand this need, most are still not aggressively pursuing competency and efficiency regarding transitions of care. Evidence of this are persistently high hospital readmission rates, low rates of successful discharge to home, and an almost complete failure to embrace and structure the consumers’ continuum of care.

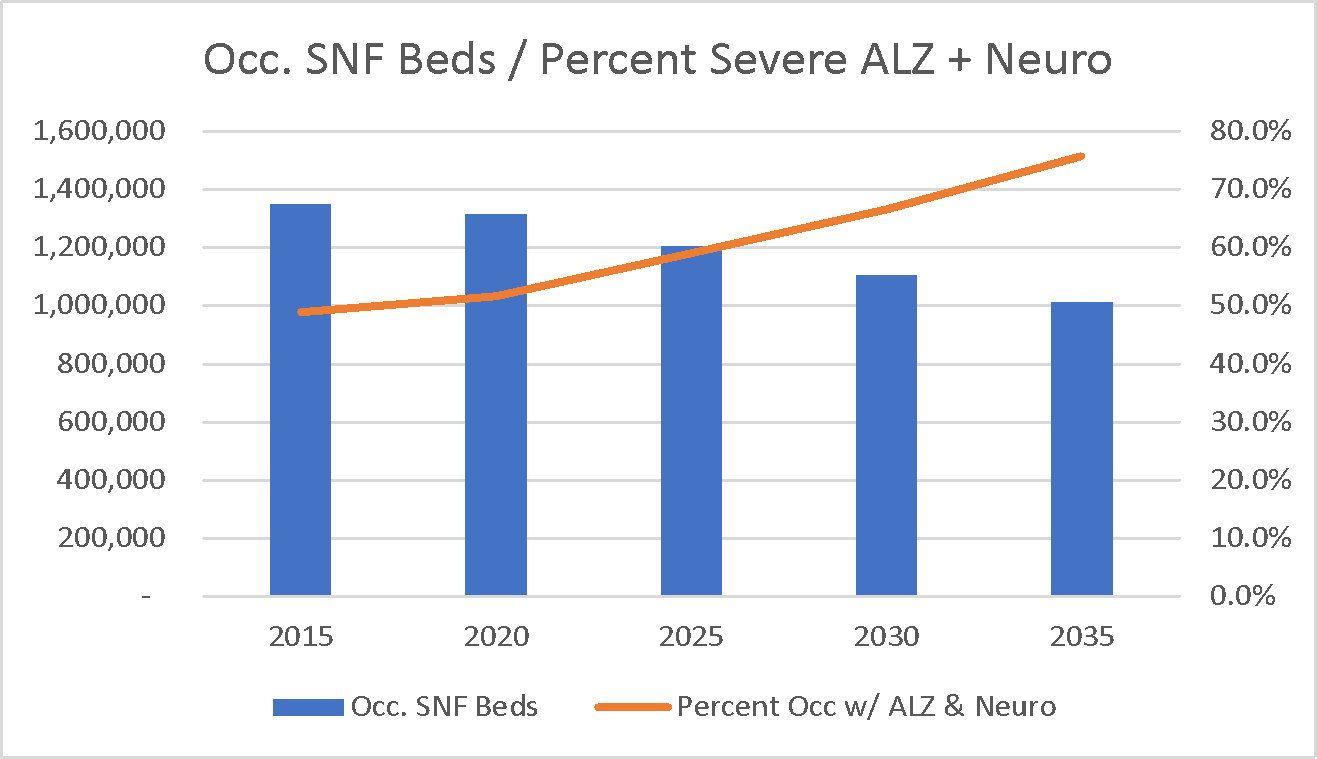

Custodial care: The other enduring need is competent custodial care. There is a certain percentage of the population, for example with third or fourth stage dementias, as well as neuromuscular/neurodegenerative disorders, which means they cannot be cared for in their residences. This baseline need (demand) is headed toward an inflection point where the contracting supply of SNF beds may not be able to meet growing demand.

While this demand/supply relationship is critically important to providers, it is unlikely that policymakers in the current political environment will pay attention.

There are other niche opportunities for nursing homes within selected marketplace areas, or for treatments of particular disorders. Niche services such as dialysis, behavioral/mental health, care for COPD, orthopedics etc. will not “fill buildings,”\ but may allow particular nursing homes to survive.

The future

Nursing homes will continue to close, the current buildings will become progressively more custodial, and in some locations, short-term rehab devoted to care transitions will continue. Nursing homes in rural areas and some ex-urban areas will disappear. There will be more leakage from nursing homes to other types of congregate properties (e.g., assisted living), resulting in gradually more medicalization of the current seniors’ housing and assisted-living inventory, with higher acuity consumers occupying units that used to be “active adults.”

Hospitals will show progressively greater interest in nursing homes as a functional part of their ecosystems, but will avoid financial or strategic entanglements with them, inhibited in part by the (bizarre) nexus of Medicare / Medicaid anti-fraud and abuse laws and Stark regulations.

By 2035, remote, personal or ambient digital technologies will have disrupted transitions of care. The “hospital at home” movement and ambient (remote) patient monitoring technologies will reduce the need for SNFs to manage post discharge populations. Demand for custodial care for the most dependent 85+ population will be surging, and there will be a call for new, congregate solutions.

This isn’t grim; it is logical. Do you see a place for your skills and competencies in this future?

We hope you do!

Irving Stackpole is president of Stackpole & Associates, a marketing, market research and training firm.

John Sheridan is Vice President Quality Analytics at CommuniCare Health Services in Cleveland, OH.

The opinions expressed in McKnight’s Long-Term Care News guest submissions are the author’s and are not necessarily those of McKnight’s Long-Term Care News or its editors.

Have a column idea? See our submission guidelines here.